Short Sellers Increase Bets Against US Life Insurers Over Private Credit Exposure

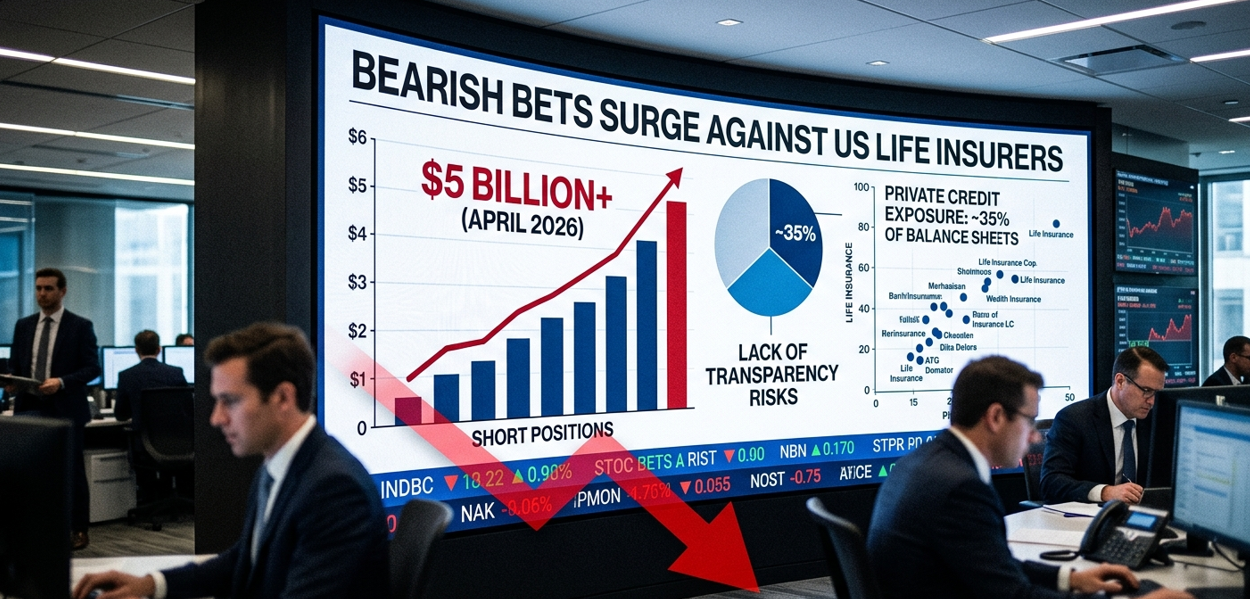

Investment firms and hedge funds are ramping up bearish positions against major US life insurers, with short interest exceeding $5.3 billion as of late April 2026. The growing concern is not related to traditional insurance liabilities, but to the asset side of insurer balance sheets.

Over the past decade, insurers have gradually shifted allocations from low-yield government bonds toward private credit markets to improve returns. However, these private loans are largely opaque, illiquid, and not publicly traded, making it difficult to assess their true market value.

Short sellers argue that in the event of an economic slowdown, rising defaults in private credit could expose hidden losses within insurer portfolios. This has raised expectations of increased regulatory scrutiny on private asset exposure and potential volatility in major players such as Principal Financial Group.